After a year and a half of misery, things are looking up for the Canadian and U.S. economies. The stock markets are up over 70 per cent from their lows of March 2009, both economies put out five per cent annualized growth rates in the last quarter of 2009, and consumer spending is on a tear. In Canada, consumer spending rose at a four per cent annualized rate in Q4 2009 and in the U.S., spending was up 1.6 per cent month to month in March, including a whopping one per cent due to sales of autos and parts alone. Economists and governments are now debating the sustainability of such encouraging results as they plan monetary and fiscal policy for the year to come.

The key question is how solid consumer finances are and how sensitive they may be to increases in interest rates, taxes, essential purchases such as gasoline prices, or a combination of all three. At its high in 2008, consumer spending accounted for nearly 70 per cent of Gross Domestic Product (GDP) in North America, so the durability of these improving retail numbers is key to predicting future economic growth overall.

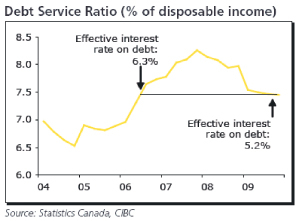

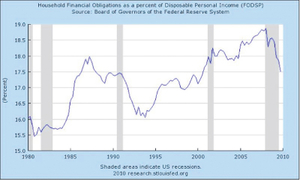

The mindset of consumers is difficult to predict, but it is fair to say that the U.S. consumer has been through a much worse credit and spending crunch than their Canadian counterparts. Comparing the two graphs here, the first one looks at Federal Reserve statistics detailing U.S. consumer debt servicing obligations when compared to income, the second from CIBC is the Canadian equivalent. Even after the recession, the U.S. consumer supports twice the cash flow burden to service their debt than the Canadian – even though the U.S. debt service requirement has fallen back to year 2000 levels, while in Canada it has only retrenched to year 2006 obligations. Some of this can be explained by U.S. mortgage interest debt deductibility that encourages U.S. consumers to pile debt on their houses to get the tax break, but it demonstrates that the U.S. consumer is still more at risk to rising interest rates and taxation encroachment than we are in Canada.

The mindset of consumers is difficult to predict, but it is fair to say that the U.S. consumer has been through a much worse credit and spending crunch than their Canadian counterparts. Comparing the two graphs here, the first one looks at Federal Reserve statistics detailing U.S. consumer debt servicing obligations when compared to income, the second from CIBC is the Canadian equivalent. Even after the recession, the U.S. consumer supports twice the cash flow burden to service their debt than the Canadian – even though the U.S. debt service requirement has fallen back to year 2000 levels, while in Canada it has only retrenched to year 2006 obligations. Some of this can be explained by U.S. mortgage interest debt deductibility that encourages U.S. consumers to pile debt on their houses to get the tax break, but it demonstrates that the U.S. consumer is still more at risk to rising interest rates and taxation encroachment than we are in Canada.

Canadians need to be seriously concerned about U.S. consumer debt levels because our economies are so intertwined. If the U.S. consumer retrenches, then the slowing effect on their economy will certainly be felt by Canadian exporters. The Canadian manufacturing sector is already struggling with the Canadian dollar at par with the U.S. greenback and most economists believe that it will stay there, or even increase in value over the next six months. Any renewed decline in U.S. spending, which could be induced by higher gas prices, a renewed slide in home prices or rising state and federal taxes, would curtail U.S. consumption of Canadian goods and services and further damage Canadian tourism, which is already reeling from the recession and a huge drop in cross-border trips by Americans.

Canadians need to be seriously concerned about U.S. consumer debt levels because our economies are so intertwined. If the U.S. consumer retrenches, then the slowing effect on their economy will certainly be felt by Canadian exporters. The Canadian manufacturing sector is already struggling with the Canadian dollar at par with the U.S. greenback and most economists believe that it will stay there, or even increase in value over the next six months. Any renewed decline in U.S. spending, which could be induced by higher gas prices, a renewed slide in home prices or rising state and federal taxes, would curtail U.S. consumption of Canadian goods and services and further damage Canadian tourism, which is already reeling from the recession and a huge drop in cross-border trips by Americans.

In a conversation with Benjamin Tal of CIBC World Markets, he emphasized that the U.S. was the only western economy to undergo a serious restructuring following the financial crisis of 2008; Canada endured a far milder recession and our banking sector was fundamentally sound, while the Eurozone is in complete denial of its structural problems and is now working on bailouts for its weakest members, like Greece. U.S. debt levels remain elevated, but the federal government has been able to fund its massive deficits because non-government credit requirements have fallen dramatically, more so than the $30-billion per week (yes, per week) that the U.S. federal government borrows on the open market. The U.S. banks have been using savings deposited with them from newly conservative American savers to purchase U.S. treasuries to fund the debt, along with China and other international investors who still view the U.S.D. as the world reserve currency.

The greatest danger is posed by rising interest rates – consumers are going to have to adjust from the environment of almost-free money that existed in the U.S. for over a year as well as record low rates in Canada. The most interesting contrast between U.S. and Canadian consumer behaviour is that U.S. consumers are deleveraging (shedding debt) while the Canadian consumer debt is at record levels, and indeed never fell during the current recession. The U.S. housing market has seen a price decline of 30 per cent overall, while Canadian prices have recovered to peak levels.

Many economists believe that the Canadian housing market has yet to face its day of reckoning, and if prices drop more than 10 per cent in hot markets like Vancouver and Toronto, a lot of consumers will find themselves unable to refinance their entire mortgage debt when it comes due. The U.S. mortgage shakeout is not over, but these properties will eventually find buyers since pricing has corrected, while a default property in Canada is going to be priced closer to the elevated pricing levels in its market and will be harder to move.

Another danger to the consumer is the impending revaluation of the Chinese Yuan, which some experts estimate is undervalued against the U.S.D. by as much as 40 per cent and must be allowed to rise in value. An appreciating Yuan means that prices for millions of consumer goods produced in China and purchased here must rise accordingly, and many of these goods are basic, weekly staples in our shopping baskets.

In the last few weeks, owners of the Dollarama chain of discount stores easily sold $250 million of shares on the open market – all based on the assumption that the low prices that attract consumers to its Chinese-made goods can be maintained. Dollarama has already moved some goods to the $2 per item price level from $1, and even if the Chinese allow only a 10-15 per cent rise in the Yuan, it will mean that Dollarama, Wal-Mart and others will have to raise prices across the board to maintain their margins. If the typical weekly Wal-Mart shopper sees their checkout receipt rise by only $10 per week based on their Chinese goods, this works out to about the price of a tank of gas a month, or $520 per year. The devastating effect of the Yuan appreciation on consumer discretionary spending should not be underestimated.

The U.S. may name China as a currency manipulator due to Chinese government reluctance to re-price the Yuan. This creates the potential for an open trade war between the two nations and a cooling of world trade, which up until now had rebounded strongly. Trade wars destroy job creation, create economic inefficiencies and ultimately limit the income growth and wealth creation needed to prolong the recovery. Thus, the U.S. has set itself up for a set of poor outcomes – if the Yuan rises too rapidly (i.e. faster than the gradual increase the Chinese are prepared to offer) the North American consumer is going to be whacked by price increases and an uptick in the inflation rate. If the Yuan does not rise, then a trade war could erupt that may derail the worldwide economic recovery with implications far beyond our own shores. Backroom negotiations are now underway to seek a compromise that allows the Yuan to rise enough to placate critics in the U.S. Congress but not so fast as to damage consumer purchasing power.

In short, the consumer has staged a great comeback but is winded by the journey. Wealth creation and income growth are critical to sustain the current advance, and the consumer faces a headwind of rising interest rates, taxes and prices over the next 12 months. It is for this reason that Ben Bernanke of the U.S. Federal Reserve and our own Mark Carney, Governor of the Bank of Canada, emphasize that while current data is encouraging, they are still cautious in their outlook and urge governments to practice restraint as they seek new sources of revenue.

Governments can expect great resistance from taxpayers who distrust expensive new spending initiatives. The consumer will seek to protect his or her house first before they willingly send more funds to meet the needs of the collective, and justifying these tax increases will prove difficult and divisive for some time to come.

Comments

Please login to post comments.